RF Insights: January Market Update

Grayson Daniels, VP of Grain Sales and Procurement, provides a Market Update for January.

.avif)

Rice Fundamental Highlights

- The January WASDE report made significant changes to several components of the long grain balance sheet. Imports were reduced another two million bushels, but exports were reduced about 11 million bushels.

- Yield and production were increased slightly, but domestic use/residual was increased 11 million bushels. As a result of all changes this month projected ending stocks were reduced 5 million bushels to 77 million bushels.

- Export demand remains poor for rough rice while continued sales to Iraq provide a good base for milled rice exports.

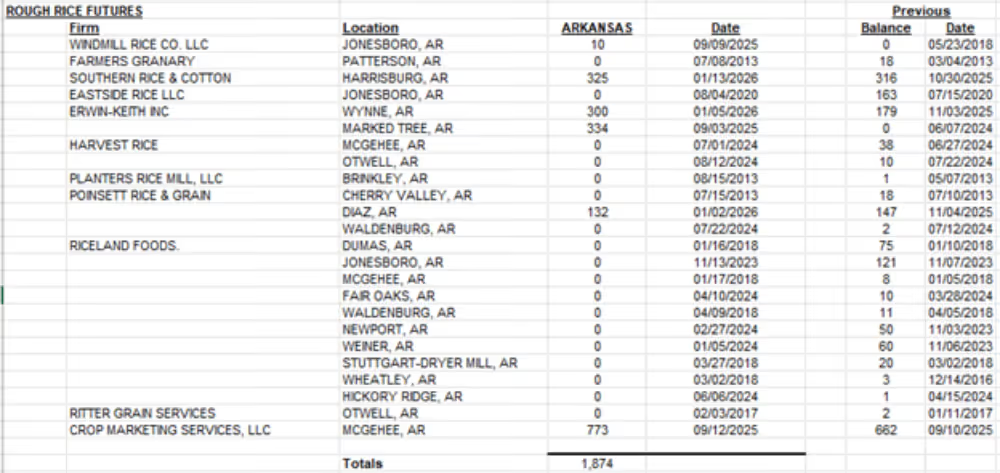

- CBOT receipts are up to 1874.

- Crop returns still indicate rice acres will decline again in 2026 which could provide the fundamental input needed for the markets to rally.

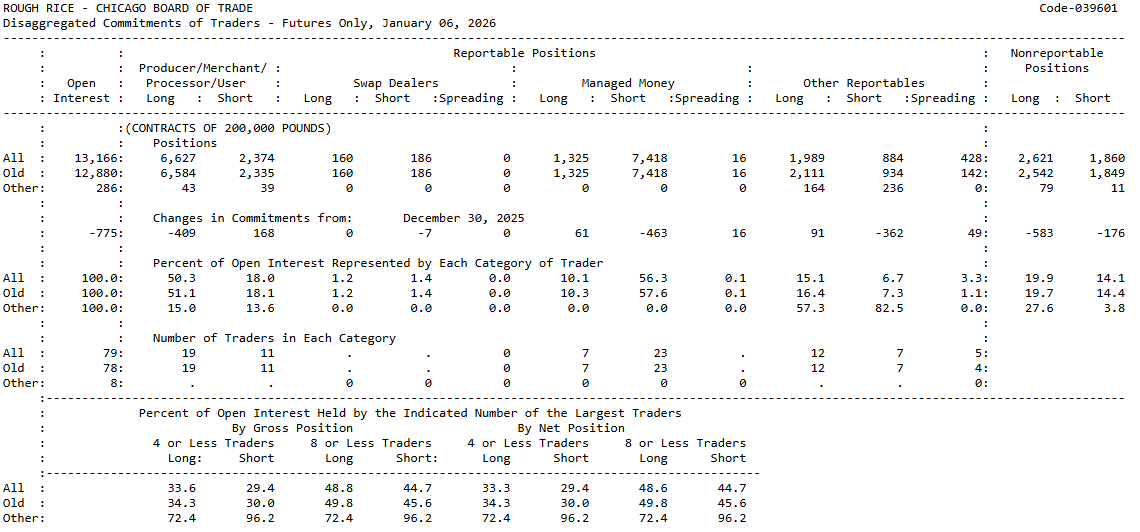

- CFTC Commitments of Traders still show the fund segment is net short approximately 6,000 contracts, however some traders in the category are increasing long positions and trade activity this week likely will show the net short position declining. Commercial positions have carried a significant net long which could likely decrease this week.

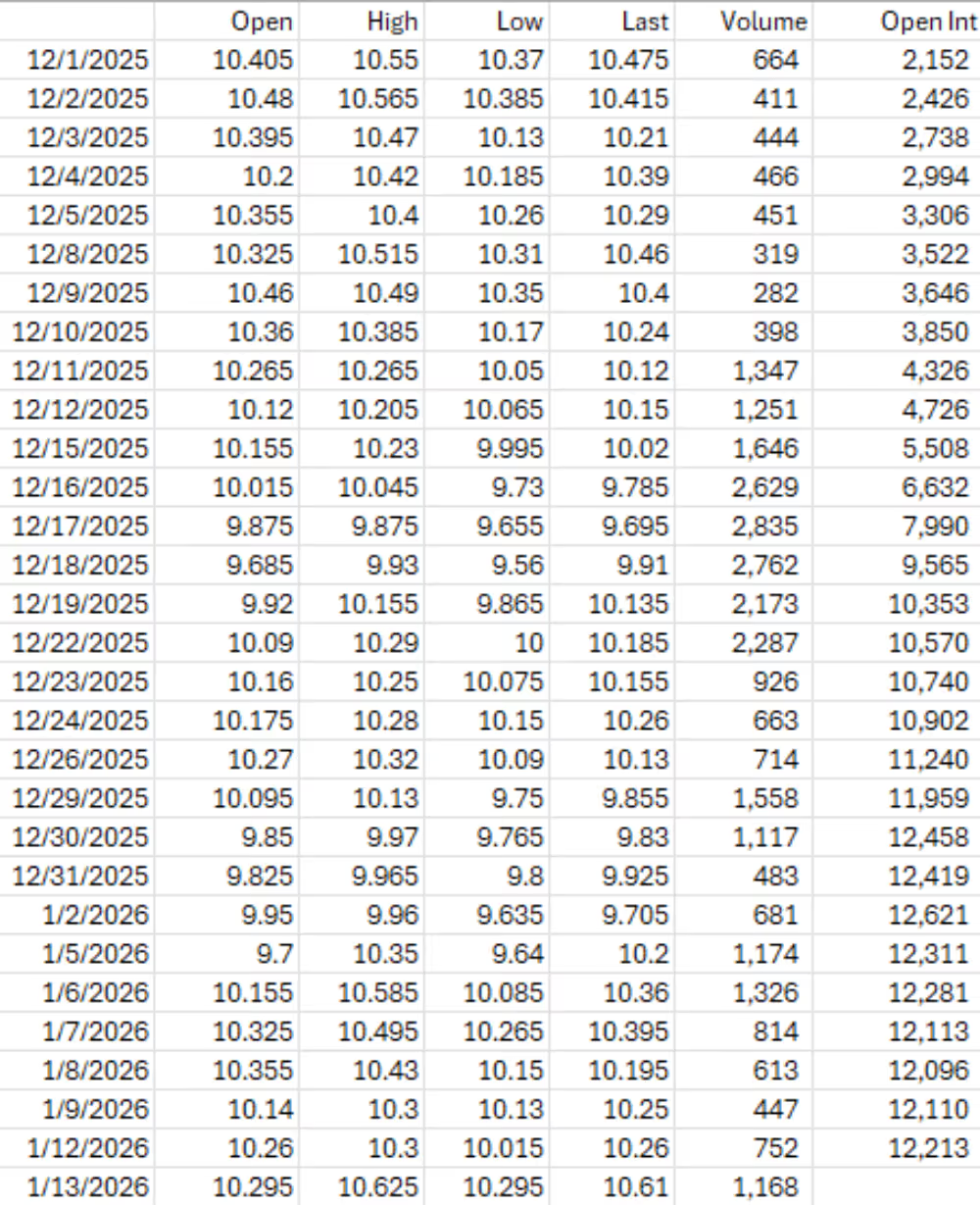

Old Crop Rough Rice Futures

Key:

Orange Line: 9-day moving average

Blue Line: 27-day moving average

CBOT Receipts As of 1-13-26

CFTC Commitments of Traders

Soybean Fundamental Highlights

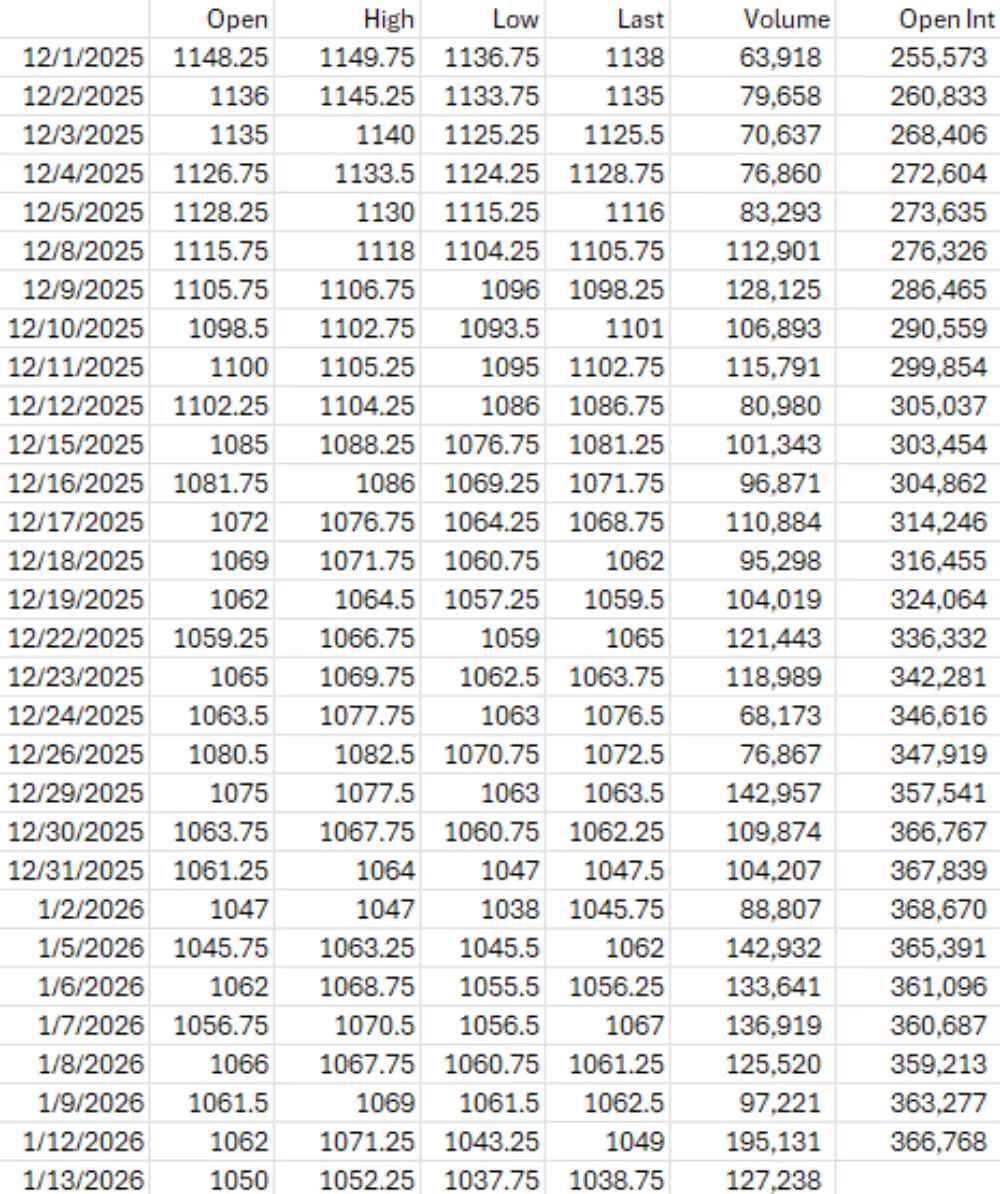

- The January WASDE made significant changes to the soybean balance sheet. Beginning stocks and production were increased slightly but exports were reduced 60 million bushels compared to last month’s projections.

- Ending stocks were raised from 290 to 350 million bushels.

- The market continued its bearish trend after the disappointing report.

- China appears to have purchased around 10 million metric tons out of the 12 million agreed to in the recent trade deal. The remainder of purchases may be spread out through the spring of 2026.

- Uncertainty regarding biofuel policy, also remains a drag on the soybean complex. RVO proposed volumes from EPA were better than expected, but they continue to delay the rule finalization. Current expectations are that EPA won’t finalize the rules until March. Finalized details of the 45Z biofuel tax credits are also lacking.

- South American weather and U.S. planting intentions will be key market drivers as we start the 2026 calendar year.

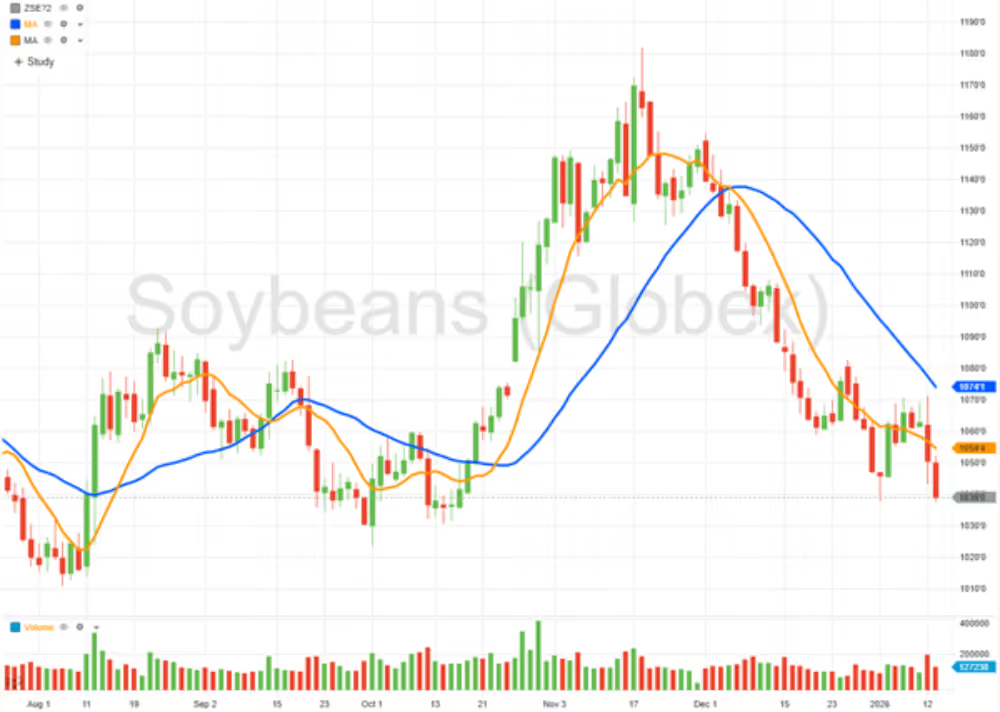

Old Crop Soybean Futures

Key:

Orange Line: 9-day moving average

Blue Line: 27-day moving average

CBOT January ’26 Soybean Values, 12/1/25 through 1/13/26

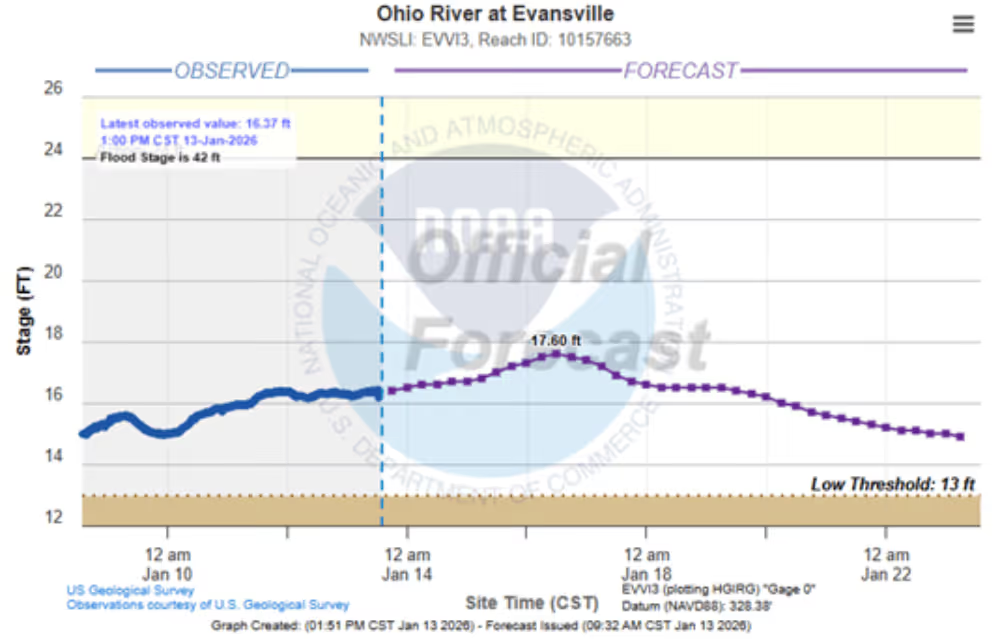

River / Weather

The Mississippi and Ohio River graphs show abnormally low levels for winter and will continue to drop without significant rain.

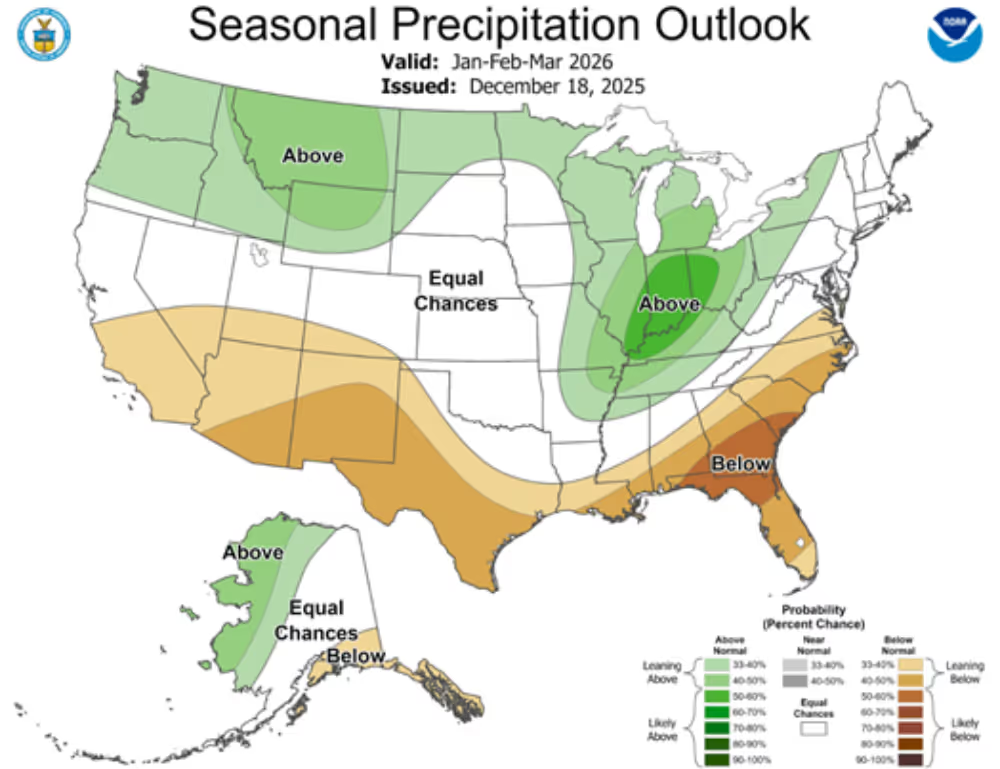

The near-term precipitation outlook shows little rain for Arkansas and Southern Missouri, however, the forecast for the last half of January shows potential for above normal precipitation. The long-term precipitation for the spring also shows above normal precipitation is possible, especially in Northeast Arkansas and Southeast Missouri. Temperatures are expected to be above normal for the next couple weeks, with the long-term outlook showing mostly normal temperatures for the spring.

NWS 7 day Precipitation Forecast

NOAA Precipitation and Temperature General Outlook