RF Insights: July Market Update

Grayson Daniels, VP of Grain Sales and Procurement, provides a Market Update for July.

Rice Fundamental Highlights

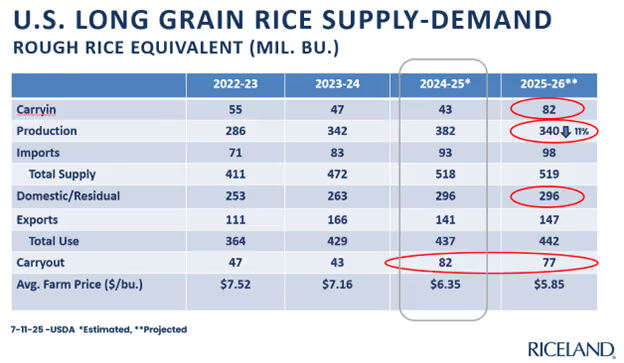

- USDA July 11 WASDE made only small changes to the old crop balance sheet (lowering exports and increasing ending stocks) and lowering the projected season average farm price for long grain to $6.35/bu.

- USDA made significant changes to new crop, lowering production as expected, due to the lower acres, but also lowering domestic use and exports. As a result of the changes, new crop ending stocks were projected at 76.9 mil. bu. despite the production decrease.

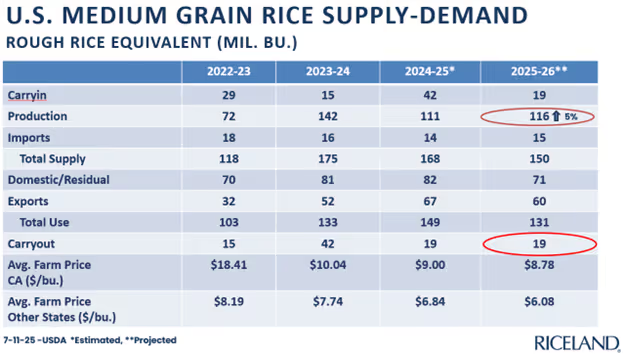

- WASDE showed overall Medium Grain production to be up 5% compared to 2024.

- Medium Grain ending stocks for 25/26 are projected at 8.8 mil. bu., a slight decrease from the current year.

- USDA continues to forecast higher imports for both long and medium grain.

- Long grain rough rice exports continue to drastically lag year-ago levels.

- Long grain milled rice exports are down slightly compared to year-ago levels.

- World rice stocks are projected to be ample, forecast at 187 million metric tons, nearly the same as the current year.

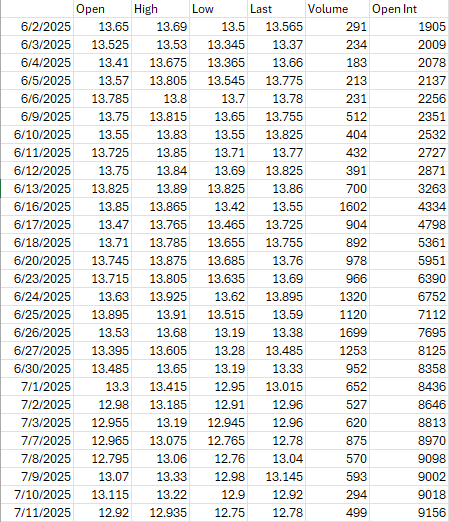

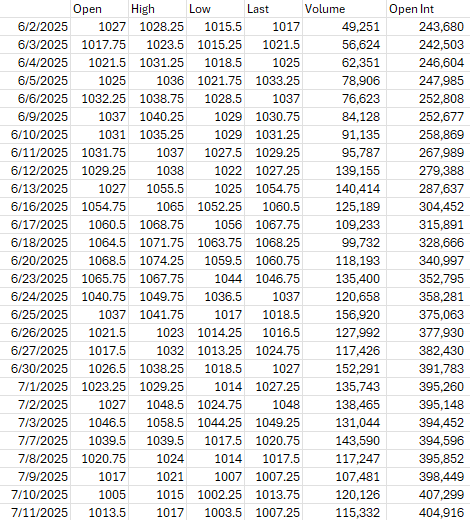

September ’25 Rough Rice Futures

Key:

Orange Line: 9-day moving average

Blue Line: 27-day moving average

CBOT September ’25 Rough Rice Values, 6/2/25 through 7/11/25

U.S. Long Grain Rice Supply-Demand

U.S. Medium Grain Rice Supply-Demand

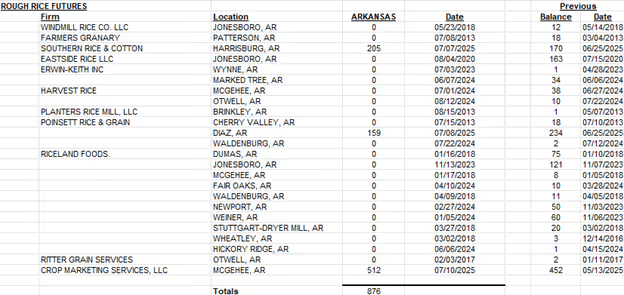

CBOT Receipts As of 7-11-25

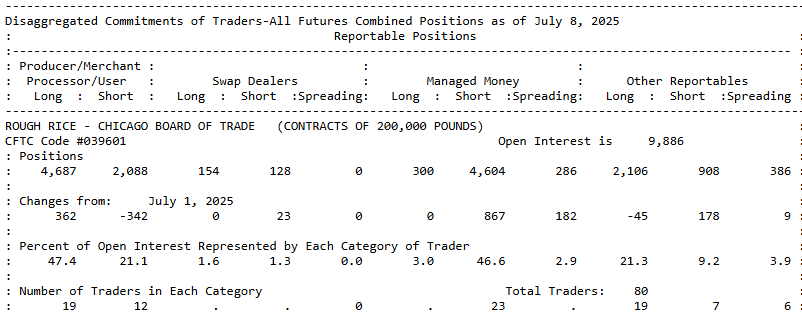

CTFC Commitment of Traders

Rice Market Summary

September futures have shown high volatility in recent weeks. As fund traders continue to sell and commercial traders continue to buy. Prices were higher in June but have struggled so far in July. The June 30 Acreage Report did not show as big of a long grain acreage reduction as most in the trade expected. The wet weather during planting season this year was similar to 2019, that year the June Acreage report showed 2,057,000 acres of long grain, however the final planted acreage that year was 1,778,000. Additional production cuts are likely, perhaps not as drastic as in 2019.Export demand needs to improve before traders are likely to get bullish.

CBOT receipts stand at 876 as of 7/11/25, all in McGehee, Diaz, and Harrisburg.

Soybean Fundamental Highlights

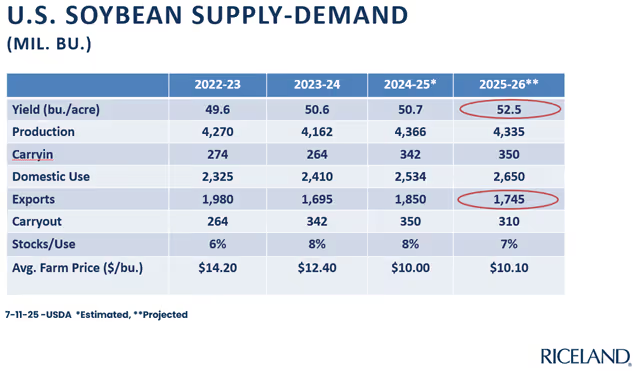

- The July 11 Supply and Demand report from USDA left old crop ending stocks unchanged at 350 mil. bu. The projected average price for old crop was increased to $10.00.

- The projected ending stocks for new crop increased slightly from 295 mil. bu. to 310 mil. bu. after decreasing production, increasing crush and lowering exports. The projected season average price for new crop was reduced to $10.10.

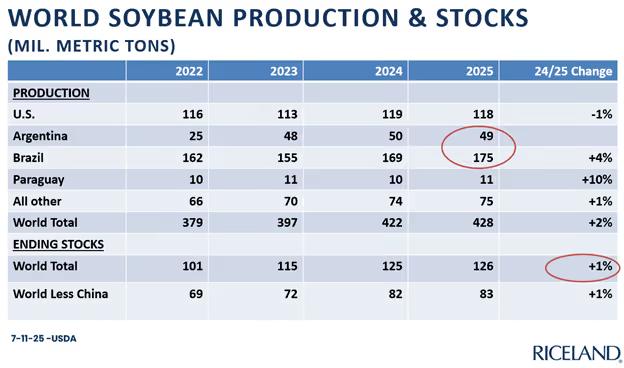

- World soybean stocks are projected to remain nearly flat after a few years of significant increases.

- The soybean market has fallen substantially in recent weeks as weather problems are minimal and trade issues remain.

- Traders will be focused on U.S. weather and tariff/trade developments with China, E.U., and other countries in the coming weeks.

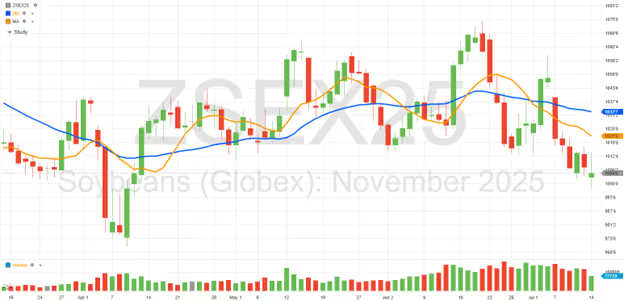

November ’25 Soybeans

Key:

Orange Line: 9-day moving average

Blue Line: 27-day moving average

CBOT November ’25 Soybean Values, 6/2/25 through 7/11/25

U.S. Soybean Supply-Demand

World Soybean Production & Stocks

Weather Outlook

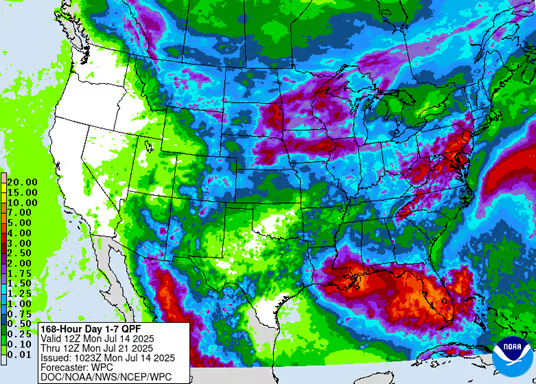

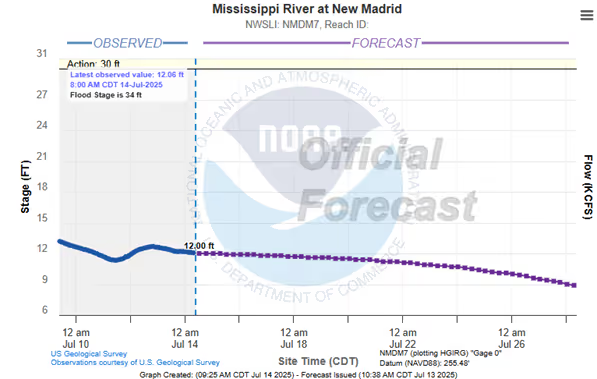

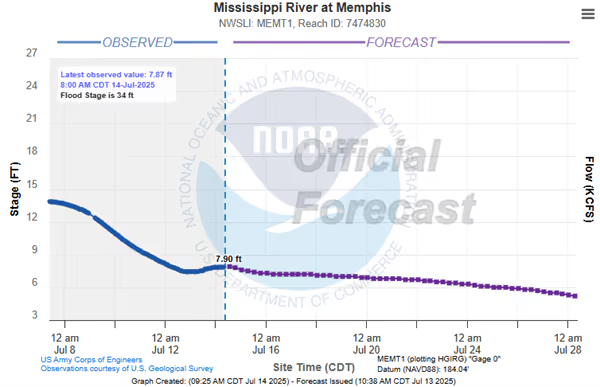

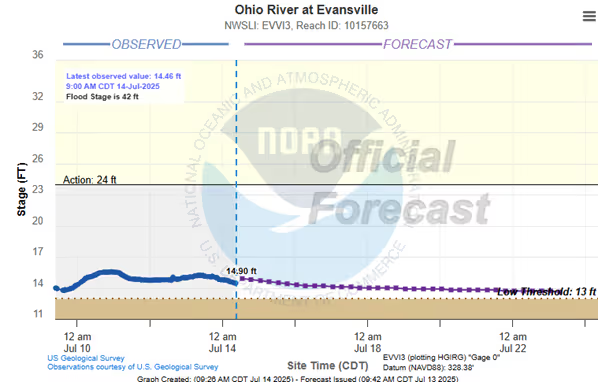

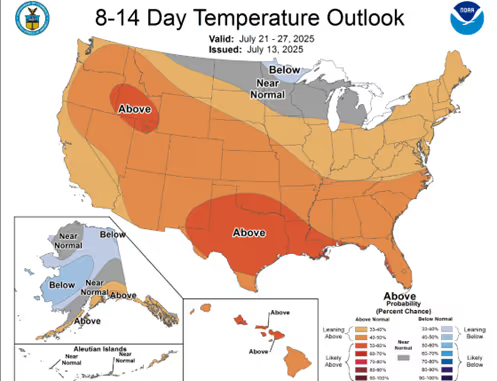

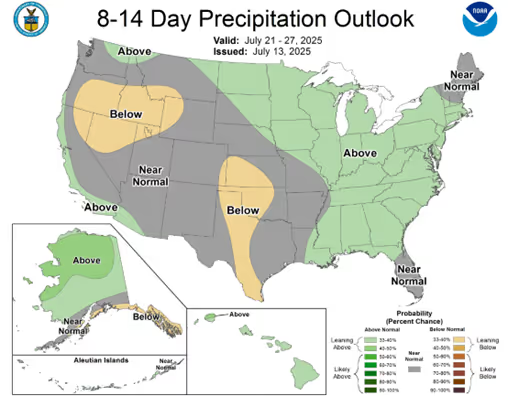

The Mississippi River and Ohio River graphs show receding levels after recent rain events, which should allow normal navigation/shipping for the next several weeks. The near-term precipitation outlook shows light rain for Eastern Arkansas. Temperatures are expected to be above normal for the next few weeks.

NOAA Temperature General Outlook

NOAA Precipitation General Outlook

NWS 7-Day Precipitation Outlook